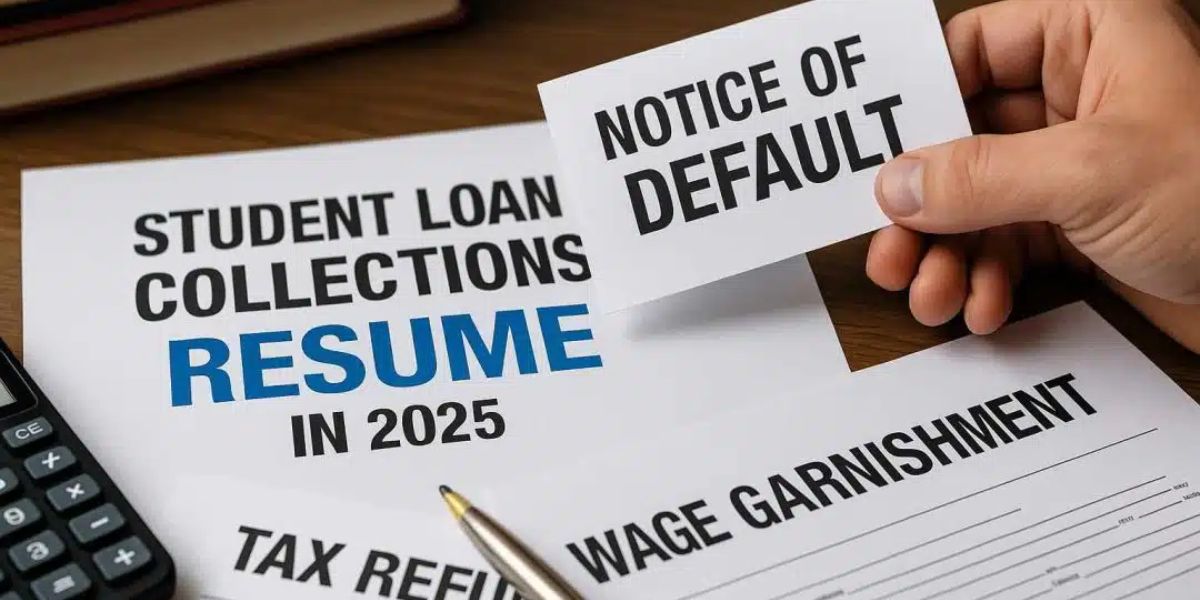

Following a five-year hiatus brought on by the COVID-19 pandemic, the federal government has restarted its efforts to collect debts owed by students who have defaulted on their student loans.

Because of the resumption of aggressive collection tactics, which include income garnishment, seizure of tax returns, and withholding of federal benefits like Social Security, millions of borrowers who have federal loans that are in default are now facing the possibility of having their payments withheld.

This action is a component of the larger efforts being made by the Trump administration to reform the student loan system and to reverse the more liberal policies that were implemented under the tenure of Vice President Joe Biden.

As the collections process is restarted, who is at risk and who is not?

The impact of this move is anticipated to be significant: about sixteen percent of borrowers of federal student loans are currently past late, and this percentage may increase as enforcement efforts become more aggressive.

Having said that, it is essential to keep in mind that not all borrowers will be affected in the same manner, and others will not be harmed at all whatsoever.

These changes do not apply to you if you are currently in possession of a private student loan.

Private loans, in contrast to federal loans, have already begun their collecting activities despite the shutdown caused by the pandemic.

It is common for private lenders to take action more quickly and aggressively when payments are missing. They frequently report the missed payments to credit bureaus within thirty days and pursue legal action in order to recover debts.

Therefore, whereas borrowers of government loans are only now beginning to feel the fresh strain, borrowers of private loans have been facing penalties for quite some time.

When it comes to federal borrowers, wage garnishment and other forms of forced collection are only applicable in the event that your loan is in default, which occurs after 270 days of nonpayment.

In the event that you are not in default, the resumed collections will not have an impact on you; nonetheless, it is still essential to keep current.

Those who are in default will be subject to enforcement through programs such as the Treasury Offset Program and administrative pay garnishment, both of which can have a significant impact on your financial situation depending on the circumstances.

To our good fortune, there are approaches to escape default

In order to rehabilitate their loans, borrowers must make nine payments that are made on time and voluntarily over a period of ten months.

On the other hand, debt consolidation may be able to pull a loan out of default, despite the fact that it may reset the progress against forgiveness.

You may be able to prevent having your wages garnished and recover access to important borrower protections such as deferral and forbearance if you take immediate action.

Read Also: Federal Government Restarts Student Loan Collections Under Trump Administration

This can be accomplished by contacting your servicer, enrolling in an income-driven repayment plan, or researching rehabilitative options.

You should verify with your loan servicer or go to the website of the Federal Student Aid program if you are unsure of the status of your loan.